For most of the past century, credit unions have been niche players in the U.S. financial services industry serving a relatively small slice of the banking market.

But in recent years, credit unions have increased their size and scope, causing commercial banks to push back and even prompting federal officials to reconsider the regulation of those institutions.

“Historically, credit unions were not seen as competitors to banks because they offered fewer small business and commercial lending products and were limited in their customer base because of field of membership restrictions,” Federal Reserve Board Governor Michelle Bowman said in a Sept. 28 speech to the Community Banking Research Conference in St. Louis.

“Credit unions today are much more likely to compete directly with traditional banks offering the full cluster of banking products and services,” she said, according to a Fed transcript of her talk.

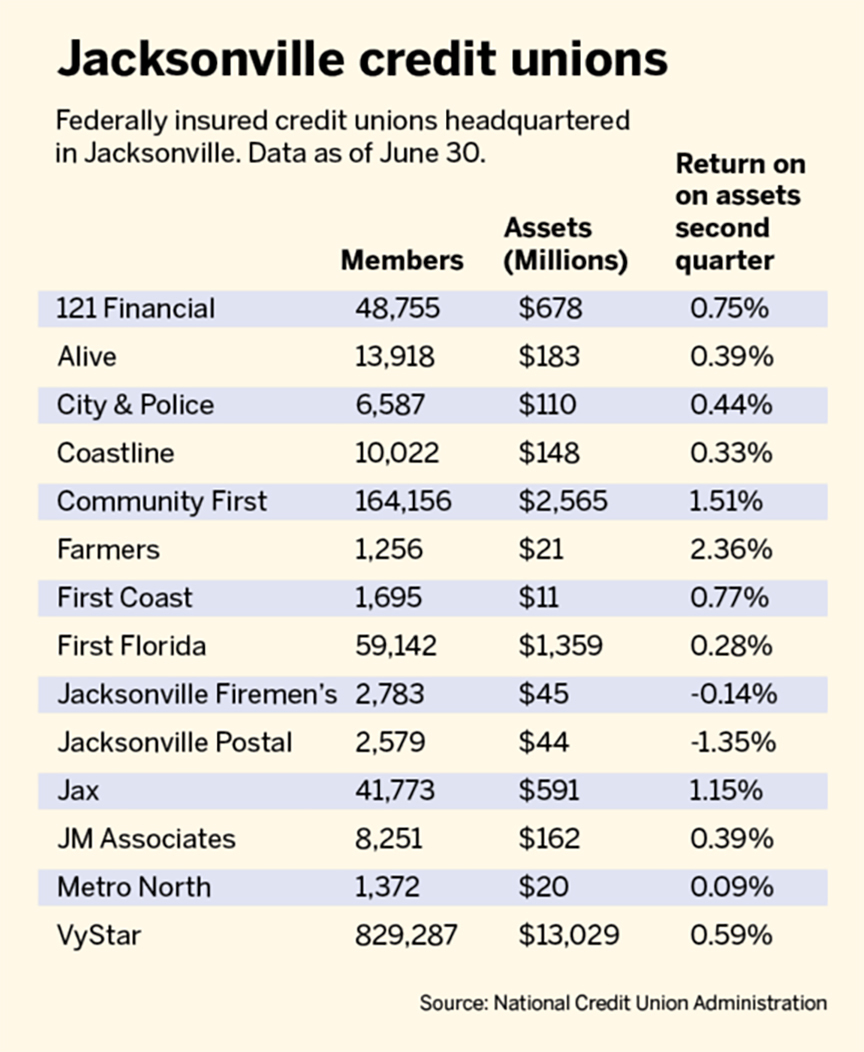

Jacksonville-based VyStar Credit Union has been at the center of the banking industry’s scrutiny over the new competition.

VyStar is the 13th largest U.S. credit union with more than $13 billion in assets and it tried to expand by acquiring a Georgia-based commercial bank, Heritage Southeast Bancorporation Inc.

Stiff opposition from commercial banks caused regulatory agencies to put off a decision on the merger application, and VyStar called off the deal in June.

According to the National Credit Union Administration, the federal regulatory agency governing the industry, credit unions are not-for-profit organizations that are designed to serve their members.

“Like banks, credit unions accept deposits, make loans and provide a wide array of other financial services. But as member-owned and cooperative institutions, credit unions provide a safe place to save and borrow at reasonable rates,” the NCUA says.

The agency says credit union profits are returned to members in the form of reduced fees and more favorable interest rates.

Credit unions began in Germany in the mid-19th century and the first U.S. credit union opened in New Hampshire in 1909.

The industry took off in the 1920s as more states enacted laws to charter credit unions.

Most credit unions served limited fields of membership, such as employees of a company. For many years, they were not considered competitors of commercial banks, which are free to solicit customers from the general public with no restrictions.

“However, in the past few decades, we’ve seen credit unions expand their fields of membership. Many credit unions now go well beyond the traditional common bond requirements for membership and increasingly allow membership based on geography,” Bowman said in her speech.

Credit unions are also expanding their services, she said.

“We’ve also seen an increase in the percentage of credit unions offering small business loans.”

Although banks are facing more competition for customers, it took the increasing trend of credit unions buying commercial banks to prompt calls for tighter regulation.

Bankers have said the tax-exempt status of credit unions allows them to offer higher prices to acquisition targets than a commercial bank could.

The Independent Community Bankers of America said in a July news release that “modern credit unions are no longer subject to any meaningful limits established by Congress to justify their tax exemption and use their tax subsidies to acquire taxpaying community banks.”

That bank trade association also said credit unions are not subject to the Community Reinvestment Act, the federal law designed to ensure banks serve their local communities.

It called on Congress to include credit unions under that law.

The National Association of Federally-Insured Credit Unions is pushing back, saying credit unions are stepping in to serve customers who aren’t getting what they need from banks.

“Banks are trying to avoid the reality that they have closed nearly 200 branches per month over the last two years, creating banking deserts in areas where Americans need financial institutions the most,” the NAFCU says on its website.

“Keeping credit unions from merging with banks and servicing these areas is both hypocritical and detrimental to the financial stability of many families and small businesses.”

Without taking sides in the debate, Bowman indicated banking regulators will be taking a closer look at the evolving financial services industry.

“As the nature of competition changes, it creates an opportunity for us to rethink how we evaluate bank mergers, how we define banking markets, and how we develop a more comprehensive understanding of the ways consumers and businesses access financial products and services today and how they might do so in the future,” she said.